App Store

App Store Profile

Profile Security

Security Sign Out

Sign Out

Feeds

Feeds

Articles

ArticlesPOPCATs Collapse Explained: Not a Flash Crash — A Precision Attack That Cost Hyperliquid $4.9M

Last night, $POPCAT suddenly plunged. At first glance, it looked like another routine liquidation cascade. But deeper analysis—on-chain flows, order book behavior, and liquidation paths—reveals something far more deliberate: a coordinated liquidity system attack.

And this might not be the first time — or the last.

In DeFi, risk often comes from where we least expect. Like last night’s ambush, your position can vanish in seconds, even if you did nothing wrong. In a hyper-transparent yet highly manipulable perpetual DEX environment, such events are almost inevitable.

1. Timeline: A Pre-Meditated Operation

1️⃣ Capital & address preparation (13 hours before crash)

The attacker withdrew $3M USDC from OKX and split it into 19 addresses.

Purpose: evade risk controls and disguise total position size.

2️⃣ Building massive long exposure

He continuously opened longs on POPCAT via Hyperliquid (HL), growing exposure to $20M–$30M — enough to move the market.

3️⃣ Creating false depth: a $30M buy wall at $0.21

He placed an enormous buy wall to simulate organic demand, luring retail traders and algos into going long. The illusion of “strong support” strengthened confidence.

4️⃣ Retail and quant traders followed the bait, assuming smart money was accumulating.

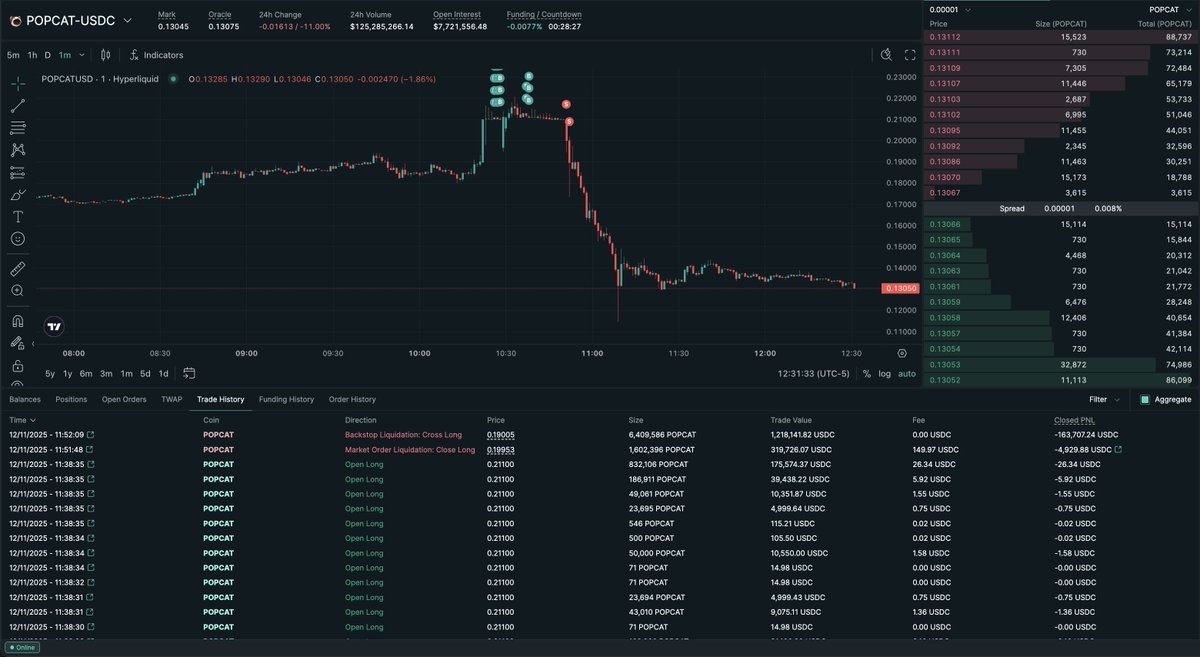

5️⃣ Instant buy wall removal → structural collapse

Without warning, he removed the wall. POPCAT’s thin liquidity couldn’t absorb the impact—price free-fell instantly.

6️⃣ Self-liquidation → collateral wiped

His own long positions were liquidated. The $3M collateral went to zero—intentionally.

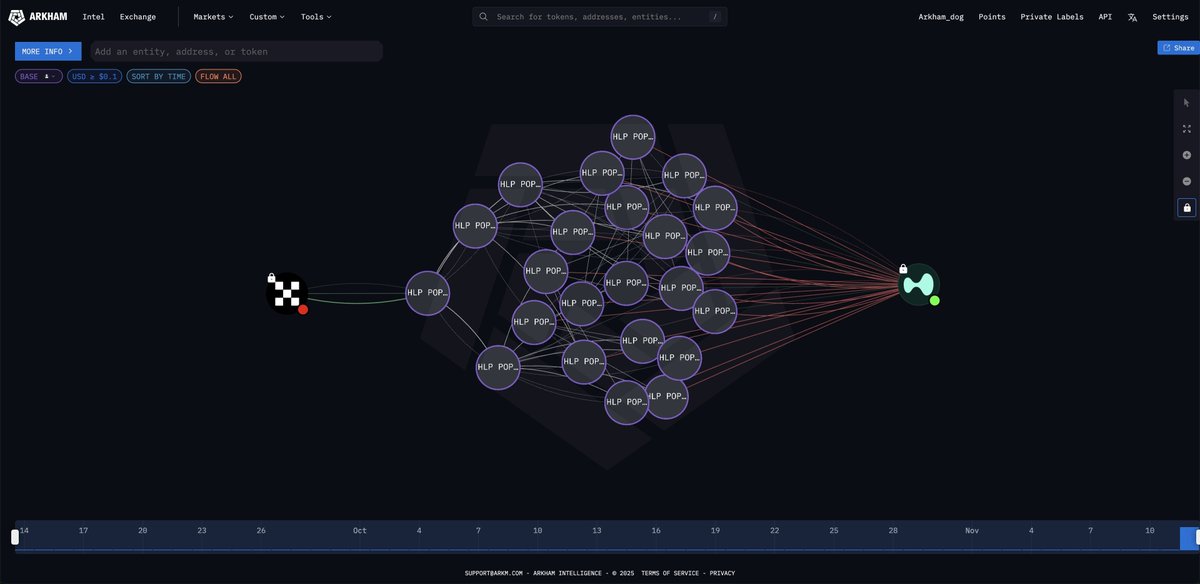

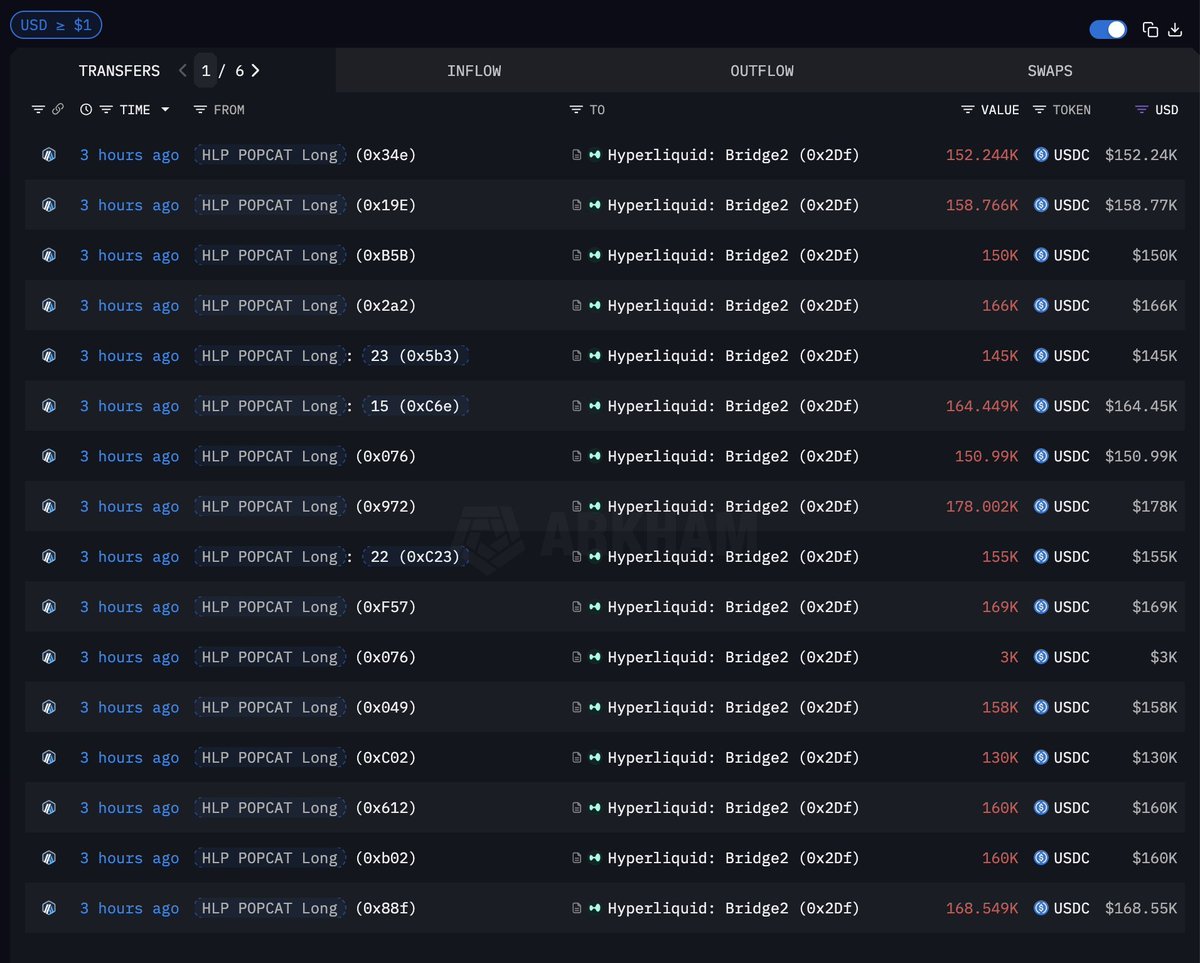

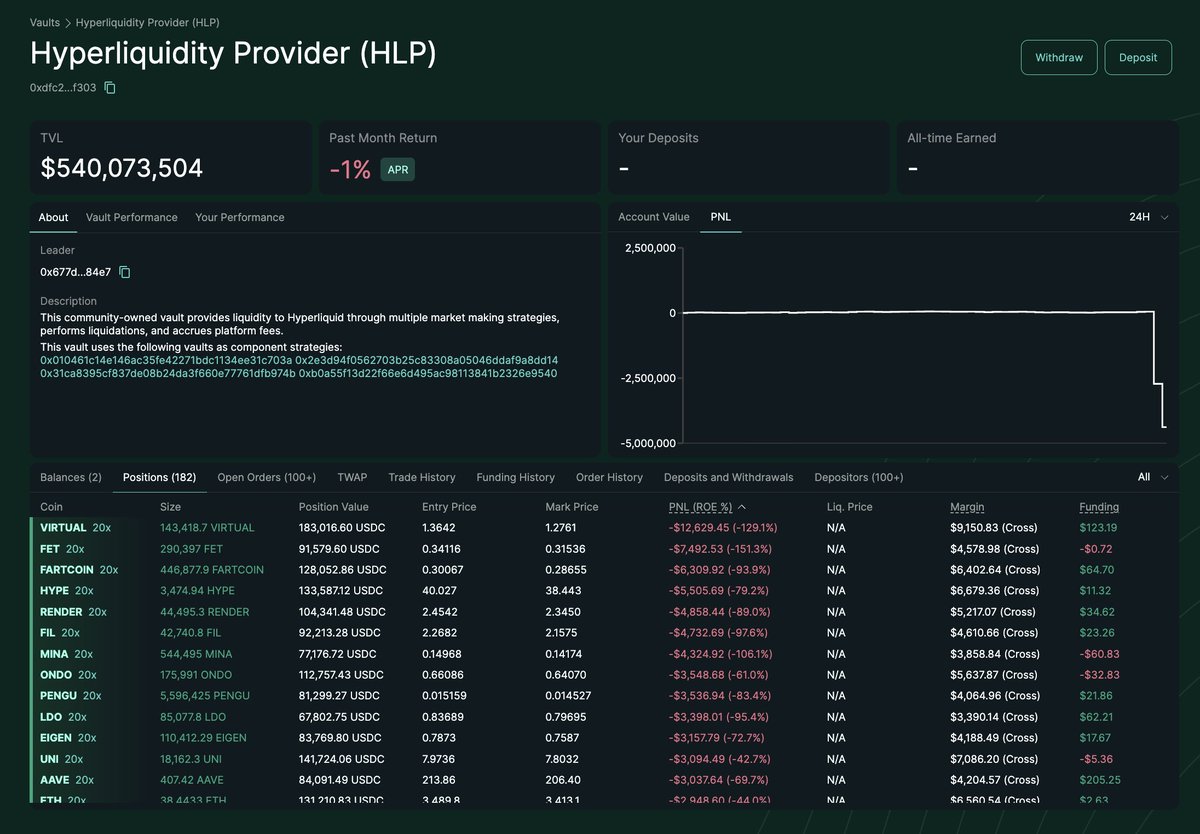

7️⃣ HLP (liquidity pool) absorbs bad debt → $4.9M loss

Because the attacker’s liquidation size far exceeded available depth, losses transferred to the protocol’s LP (HLP), which automatically absorbed the shortfall.

8️⃣ Hyperliquid intervened manually, closing residual risk.

9️⃣ The Arbitrum bridge was briefly paused (intra-exchange deposits/withdrawals unaffected).

In short:

He used real capital as bait, manipulated visual liquidity, exploited liquidation slippage, and forced the platform to eat the loss.

That’s the core vulnerability of perpetual DEXs.

2. Why This Wasn't a "Normal Liquidation"

Key clues:

19 split wallets → professional prep

Massive fake buy wall → intentional trap

Sudden removal triggering chain liquidations → deep mechanism knowledge

Zeroed collateral → planned sacrifice

Third major incident on HL → consistent pattern

This was not a trader gone wrong — it was a deliberate system-level arbitrage, using fake depth to trigger cascading liquidations and shift losses to LPs.

3. The Structural Weakness of Perp DEXs

The significance isn’t the $4.9M loss—it’s the revelation of a repeatable attack vector.

Decentralized perpetual protocols share the same structural flaw:

Low liquidity + High leverage + Orderbook dependency = Attack surface.

1️⃣ Low-liquidity assets (long-tail tokens like POPCAT) → cheap to manipulate.

2️⃣ High leverage (20–30x) → amplify small price moves exponentially.

3️⃣ Clearing relies on order book depth → manipulate depth, break liquidation path.

Combine all three, and the system becomes exploitable.

GMX, Drift, MUX, Vela, even early dydx—all have faced similar issues.

It takes only hundreds of thousands to trigger millions in losses, posing long-term risk across the Perp DEX sector.

4. Lessons and Takeaways

Perp DEXs like Hyperliquid exploded in popularity for transparency and on-chain fairness.

But transparency also means predictability, and predictability invites exploitation.

For traders:

Long-tail assets are easiest to manipulate.

On-chain buy/sell walls are never reliable.

Volatile markets attract manipulators.

Risk lies not only in price but in system design.

For LPs:

Perp DEX yield = counterpart risk.

Where leverage exists, bad debt will follow.

HLP/GLP/vLP = liquidation counterparties.

Extreme moves can impose asymmetric losses.

For the industry:

This will push protocols to:

Limit tradable assets

Redesign liquidation logic

Add anti-manipulation controls

Diversify oracle price feeds

Establish insurance or backstop funds

Restrict fake depth & rapid order withdrawals

Painful, but necessary. Every collapse forces the sector to evolve.

5. Final Thoughts: You Can’t Predict Risk, Only Yourself

POPCAT’s plunge was just one price move—but its design was surgical.

It reminds us that DeFi isn’t just tech—it’s a battlefield of incentives, systems, and human behavior.

The real danger isn’t market volatility. It’s when the system itself becomes the weapon.

You can’t predict where the next attack will come from—but you can know your limits.

Understand what you don’t understand. Avoid what you can’t measure.

Profit matters less than capital preservation.

Because in this market, if you don’t know where the yield—or the risk—comes from,

you are it.

Source

Source

Add to Favorites

Add to Favorites Download image

Download image Share x

Share x Copy link

Copy linkBitcoin may enter a prolonged sideways phase between $57K and $87K as markets enter a relief period following a 52% drop from ATH. This consolidation could mirror the 2022 fractal, creating liquidity before a potential breakdown toward the $44K–$50K range.

Doctor Profit/2026.03.09

Davinci Jeremie urged people to buy $1 of Bitcoin in 2013 and became a symbol of early conviction. Years later, fame, lifestyle flexing, and token promotions sparked criticism. His journey reflects both crypto foresight and influencer-era controversy.

StarPlatinum/2026.03.04

A sweeping narrative ties Jane Street to India’s expiry-day options case, alleged 10AM Bitcoin sell patterns, Terra’s collapse, and ETF plumbing. While none prove misconduct, critics argue a common structure: move spot, monetize derivatives, keep execution opaque.

Bull Theory/2026.02.27

A controversial narrative links Jane Street, ETF mechanics, and Bitcoin’s price behavior, pointing to lawsuit allegations, 10AM volatility patterns, and derivative hedging dynamics. The discussion raises broader questions about liquidity, structure, and price discovery.

Justin Bechler/2026.02.26

A new federal lawsuit alleges Jane Street exploited non-public information tied to Terraform’s liquidity defenses, accelerating UST’s depeg and the Terra collapse. The firm denies the claims. The case may reignite debates on structure, design, and regulation.

Diana/2026.02.25

Mean reversion and on-chain models sit at levels historically linked to bottom formation after capitulation. Realized losses reached record USD values, while deviations from anchor models remain extreme. Price pain may be fading; patience remains key.

Checkmate/2026.02.25

Hot feeds

A trader profits $448K by monitoring #Binance's new listings!

2024.12.13 17:37:29

Last week, funds have flowed into #Bitcoin, #Ethereum, and #Hyperliquid.

2024.12.16 14:48:36

A $PEPE whale that had been dormant for 600 days transferred all 2.1T $PEPE($52M) to a new address.

2024.12.14 10:35:27

When Elon Musk tweeted about Moltbook, the meme coin MOLT experienced a short-term 30% price surge, hitting a new all-time high of $114 million.

2026.01.31 18:37:29

A smart #AI coin trader made $17.6M on $GOAT, $ai16z, $Fartcoin,$arc.

2025.01.05 16:05:18

A sniper earned 2,277 $ETH ($8.3M) trading $SHIRO within 18 hours!

2024.12.03 23:09:08

MoreHot Articles

How did I turn $1,000 into $30,000 with smart money?

2024.12.09

10 promising AI Agent cryptos

2024.12.05

The 30-Year-Old Entrepreneur Behind Virtual, a Multi-Million Dollar AI Agent Society

2025.01.22

10 smart traders specializing in MEMEcoin trading on Solana

2024.12.09

A trader lost $73.9K trading memecoins in just 3 minutes — a lesson for us all!

2024.12.13

What is $SPORE? Let us take you through the on-chain records to show you how it works.

2024.12.25